Monday 22 June 2015

At the recent EU Sustainable Energy Week, Vice-President Maroš Šefčovič said “we should treat energy efficiency as an energy resource in its own right” and in fact the Commission now talks about energy efficiency first. Efficiency enthusiasts have long advocated this view so it is good to see it beginning to be adopted by the EC.

If efficiency is to be treated as a resource we need to map the language of efficiency onto the language of other energy resources. The energy and finance industry has its own language when taking about resources, a language that is itself often mis-understood by outsiders. In the 1970s there were many reports of oil running out based on the fact that there were only 20 (or 30 or some other number) of years of oil reserves left. This completely mis-understood the meaning of reserves. So let’s look at the language of conventional fossil fuel energy resources and how that maps onto energy efficiency.

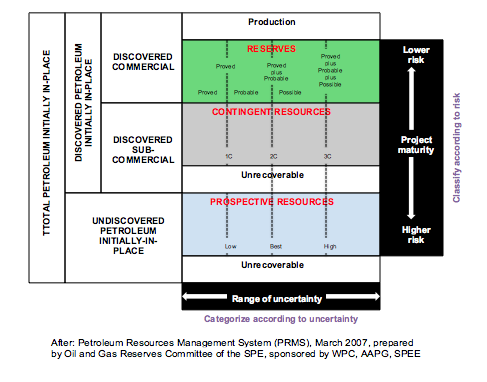

The methodology for defining and measuring resources and reserves is called the Petroleum Resources Management System (PRMS) and has been developed by the Society of Petroleum Engineers and endorsed by the World Petroleum Council, the American Association of Petroleum Geologists, the Society of Petroleum Engineers and the Society of Exploration Geophysicists. The valuation of oil and gas companies are based on the use of the PRMS and when oil and gas companies come to the public markets the price is related to the PRMS assessment as it provides a standardized way of assessing, and therefore valuing, resources and reserves.

The diagram and the text below explains the PRMS and the definitions.

RESERVES are those quantities of petroleum anticipated to be commercially recoverable by application of development projects to known accumulations from a given date forward under defined conditions. Reserves must further satisfy four criteria; they must be discovered, recoverable, commercial, and remaining (as of the evaluation date) based on the development project(s) applied. Reserves are further categorized in accordance with the level of certainty associated with the estimates and may be sub-classified based on project maturity and/or characterized by development and production status.

CONTINGENT RESOURCES are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations, but the applied project(s) are not yet considered mature enough for commercial development due to one or more contingencies. Contingent Resources may include, for example, projects for which there are currently no viable markets, or where commercial recovery is dependent on technology under development, or where evaluation of the accumulation is insufficient to clearly assess commerciality. Resources are further categorized in accordance with the level of certainty associated with the estimates and may be sub-classified based on project maturity and/or characterized by their economic status. Note that for resources to be classified as Contingent Resources they must be discovered.

UNDISCOVERED PETROLEUM INITIALLY-IN-PLACE is that quantity of petroleum estimated, as of a given date, to be contained within accumulations yet to be discovered.

PROSPECTIVE RESOURCES are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from undiscovered accumulations by application of future development projects. Prospective resources have both an associated chance of discovery and a chance of development. Prospective resources are further subdivided in accordance with the level of certainty associated with recoverable estimates assuming their discovery and development and may be sub-classified based on project maturity. Prospective Resources can be sub-classified as Prospects, Leads and Plays as follows:

- Prospect: A potential accumulation that is sufficiently well defined to represent a viable drilling target.

- Lead: A potential accumulation that is currently poorly defined and requires more data acquisition and/or evaluation in order to be classified as a prospect.

- Play: A prospective trend of potential prospects, but which requires more data acquisition and/or evaluation in order to define specific leads or prospects.

UNRECOVERABLE is that portion of Discovered or Undiscovered Petroleum Initially-in-Place quantities which is estimated, as of a given date, not to be recoverable by future development projects. A portion of these quantities may become recoverable in the future as commercial circumstances change or technological developments occur; the remaining portion may never be recovered due to physical/chemical constraints represented by subsurface interaction of fluids and reservoir rocks.

Determination of Commerciality

Discovered recoverable volumes (Contingent Resources) may be considered commercially producible, and thus Reserves, if the entity claiming commerciality has demonstrated firm intention to proceed with development and such intention is based upon all of the following criteria:

- evidence to support a reasonable timetable for development.

- a reasonable assessment of the future economics of such development projects meeting defined investment and operating criteria.

- a reasonable expectation that there will be a market for all or at least the expected sales quantities of production required to justify development.

- evidence that the necessary production and transportation facilities are available or can be made available.

- evidence that legal, contractual, environmental and other social and economic concerns will allow for the actual implementation of the recovery project being evaluated.

To be included in the Reserves class, a project must be sufficiently defined to establish its commercial viability. There must be a reasonable expectation that all required internal and external approvals will be forthcoming, and there is evidence of firm intention to proceed with development within a reasonable timeframe. While 5 years is recommended as a benchmark, a longer time frame could be applied where, for example, development of economic projects are deferred at the option of the producer for, among other things, market-related reasons, or to meet contractual or strategic objectives. In all cases the justification for classification as Reserves should be clearly documents.

The energy efficiency analogues

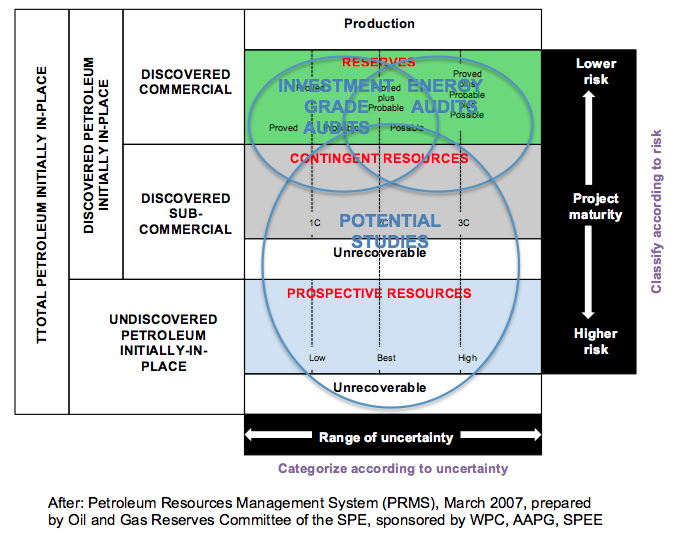

So, having explained the PRMS, what are the equivalents in energy efficiency and how do we need to change the language so that we can think of efficiency as a resource?

Clearly assets in Production are efficiency projects that have been implemented and working. Like oil fields actual production (of “negawatt hours”) will vary from the initial design estimates, this variation can be down to errors of designs (technical performance) and variations in other factors e.g. occupancy patterns in a building. The economic performance will of course be affected by the price of energy that is being “saved” which will almost certainly vary during the project lifetime, just like the price of oil varies during the production lifetime of an oil field. In both cases the only certainty is that the actual output and actual economic performance will be different to that estimated in the investment case.

Energy efficiency reserves, using the PRMS criteria of being discovered, recoverable, commercial and remaining, are those projects that have been identified in some process (probably involving an energy audit), can be implemented practically, are commercial according to the investor’s criteria and are as yet not implemented. The level of uncertainty addressed in the PRMS fits nicely with the difference between a regular energy audit or survey and an Investment Grade Audit (IGA). IGAs typically include fixed prices and a financing plan. (An IGA can be level II or III in ASHRAE or Type 3 under ISO50002.)

Also of course an audit of either type, a simple audit or an IGA, can find projects that are sub-commercial i.e. Contingent Resources. One of the definitions of sub-commercial is projects for which there are “currently no viable markets” – there actually isn’t a market for energy efficiency although we can envisage a situation where there could be, similar to the market for demand response. Creating such a market would require the appropriate regulatory framework. The other criteria is “where commercial recovery is dependent on technology under development”, in energy efficiency there are projects that are dependent on emerging technology and assumptions about its timing and/or costs and benefits. The third criteria is “where evaluation of the accumulation is insufficient to clearly assess commerciality”, i.e. the level of uncertainty is too high due to a lack of information. This may be a project identified by an audit but where there is still uncertainty over costs and savings, uncertainty that can be reduced by further measurement and analysis or cost determination, or external, contextual uncertainties e.g. uncertainty about the future ownership or occupancy of a building.

Over the last forty years there have been numerous studies of the potential for energy efficiency. One problem with these studies is the definition of economic, what is economic is defined by the investor and will vary from investor to investor. They also often cover the equivalent of Reserves, Contingent Resources, Undiscovered, Prospective Resources and Unrecoverable without breaking the potential down. The size of the Unrecoverable energy efficiency is driven by the technological frontiers with the upper limit set by the laws of thermodynamics.

It is often said that one of the problems with energy efficiency is that it is invisible. This is true but let’s not forget that oil and gas resources and reserves are also invisible, it is only the tools of geology and seismic studies – which are increasingly sophisticated – which allows us to “see” those resources. In energy efficiency it is tools like benchmarking and energy audits that allow us to see the resource.

One of the differences between energy supplies and energy efficiency is that once the reserves are identified they don’t usually sit around for many years without being developed. Compared to oil and gas the reserves are made up of many (millions of) individual small projects and implementation usually follows evaluation fairly quickly, unlike in oil and gas where projects can cost billions and take many years. On the other hand we know that there have been years of energy audits which identified economic projects which have not been implemented – energy audits are notorious for sitting on the book shelf (or these days on the hard drive). The projects identified in those audits are effectively energy reserves and contingent resources which are not valued. They have a high degree of uncertainty but they are there.

If you are an oil and gas company with control over reserves and even resources, these have a value against which you can raise money. This is how oil and gas E&P (exploration and production) companies raise money on markets like AiM (Alternative Investment Market) or TSX (Toronto Stock Exchange). Given that nearly every building has reserves of energy efficiency potential we need to think about mechanisms that value that potential, just like we value oil and gas fields before they are exploited.

The built environment is probably our biggest energy resource.

Comments

There are 3 comments on “Energy efficiency as a resource”:

Dr Steven Fawkes

Welcome to my blog on energy efficiency and energy efficiency financing. The first question people ask is why my blog is called 'only eleven percent' - the answer is here. I look forward to engaging with you!

Get in touch

Tag cloud

Black & Veatch Building technologies Caludie Haignere China Climate co-benefits David Cameron E.On EDF EDF Pulse awards Emissions Energy Energy Bill Energy Efficiency Energy Efficiency Mission energy security Environment Europe FERC Finance Fusion Government Henri Proglio innovation Innovation Gateway investment in energy Investor Confidence Project Investors Jevons paradox M&V Management net zero new technology NorthWestern Energy Stakeholders Nuclear Prime Minister RBS renewables Research survey Technology uk energy policy US USA Wind farmsMy latest entries

- ‘Here we go again’ – but this time we have a choice

- The corruption of purpose in business – and how to address it

- Gee, I wish we could have a white Christmas, just like the old days….

- A look back at the last forty years of the energy transition and a look forward to the next forty years

- Domains of Power

- Ethical AI: or ‘Open the Pod Bay Doors HAL’

- ‘This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning’

About 30 years I’ve been having this speech. Fortunately that European autoridades start to realize.

Congratulations for the excellent text, with which I agree.

João de Jesus Ferreira

Very interesting. This action is one of the things you can do in the short term. I think like that. thing to do is to create a policy that limits the household and industrial energy overload. and this can only be done with the level of public awareness is more modern. in the long term, is to find new sources and alternative uses, and accompanied by a pattern of growing industries in the future. very difficult to predict. but it is absolutely necessary and must be done by a corporation or state agencies. nice post. thanks.

[…] efficiency expert Dr Steven Fawkes thinks the industry should adopt the language of energy traders to encourage investors and banks to trade […]