Saturday 25 January 2025

The latest in a series of blogs inspired by my 1985 PhD

There have been many, many studies over the years discussing the potential for energy efficiency, in fact there are almost as many studies on potential as there are on the barriers to energy efficiency. As I sometimes joke, if I had ten pounds for each of those I could probably retire. However, very few of the studies on potential really define potential.

The question of what is the potential for energy efficiency, both the meaning and the quantum, was an important element of my research which set out to review the feasibility of achieving a low energy future. As the work progressed, it became obvious that potential, when used in anything other than its pure physical science meaning, is a ‘soft’ concept that needs to be defined. Leach et.al., in their “A Low Energy Strategy for the UK’, along with many other studies of potential made no effort to different types of potential.

Potential is not static, it is continually being altered by technological and economic developments – it is a dynamic just like reserves and resources of oil and gas. At any time, and in any particular site, and site specificness is very important, there are the following types of potential.

- There is a totally theoretical potential based on the laws of physics without any consideration of practical available technology.

- There is the potential for improving energy efficiency that derives from the physics of the process or installation using known concepts i.e. not magic, which is also a theoretical potential.

- A sub-set of this potential is the potential that can achieved by applying available, existing technology.

- This sub-set, at any one time, is further divided into potential that is economic and potential that is not economic.

It is the latter that is actionable by the firm. It can be defined as the potential resulting from those investment possibilities that:

- are capable of being developed and implemented by the host organisation (or householder) or vendor/supplier/contractor

- meet the financial criteria set by the organisation making the investment

- are appropriate in context i.e. other considerations at the time.

The schema of potentials can also be divided into that available from retro-fitting and that available from installing new plants or processes.

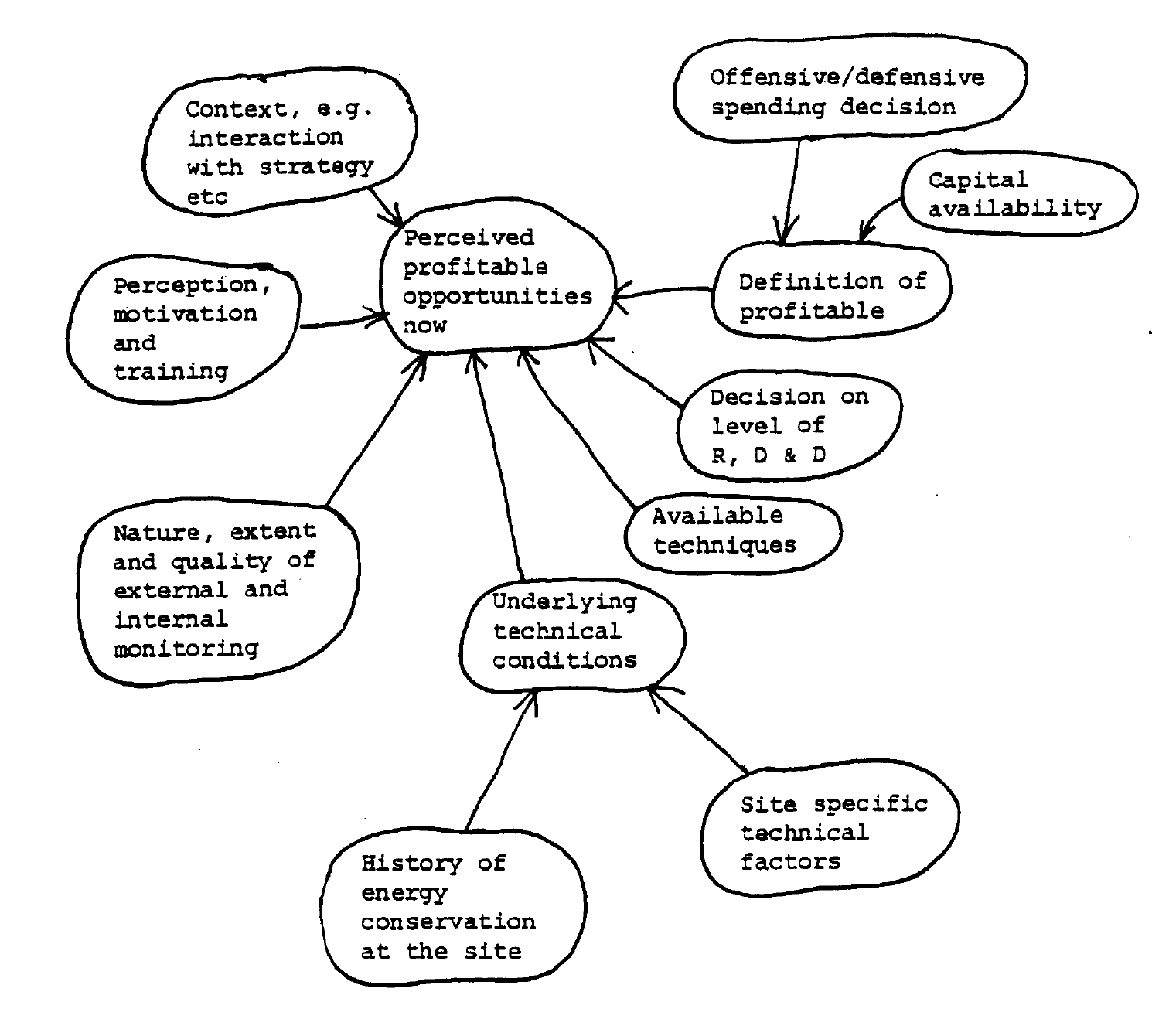

Obviously the size of the potential depends on judgements and decisions outside the usually accepted boundaries of energy management. Clearly two organisations operating similar facilities could have different investment criteria due to differing decisions on priorities for capital or differing return requirements by their owners, giving different potentials even if their underlying facilities are identical.

Furthermore, and overlaid on these potentials are the perceptions and performance of management. Differences in perceptions may come from two sources, differences in the quality of internal and external information flows, and differences in the selective perception of information by actors in the process. Internal information includes energy performance information but also other information about the wider business. External information includes many things including information on the availability of technology and hardware, and views on future energy prices. For example, in one site the possibility of a certain energy efficiency measure may not be perceived at all due to a lack of knowledge. In another similar site that particular measure may be considered unrealistic because of a prior bad experience. Such ‘biases’ are important in determining what is considered achievable and appropriate by management. Perceptions filter objective reality.

As prices and available technologies change, the potentials change. Thus any attempt to estimate or measure potential will always be fuzzy. A real measurement of potential requires blending detailed engineering work with management views and perspectives – sometimes called an Investment Grade Audit. Gathering this level of detail is an expensive exercise with an ephemeral result. It is only worthwhile going to the expense if management believe a measure is likely to be implementable and investable.

The factors that influence the potential in any one site at any point are shown in the soft systems inspired diagram.

This analysis emphasises the fact that potential for energy efficiency is analogous to that for energy resources and reserves, something that I explored in this 2015 blog, ’Energy Efficiency as a Resource’

The next time anyone talks about or writes about the potential for energy efficiency ask what is their definition of potential.

Sunday 19 January 2025

I was shocked to be reminded that that 40 years have elapsed since I finished my PhD at the University of Stirling. The thesis title was the rather ponderous, ‘The potential for energy conserving capital equipment in UK industry’, and the general research objective was to test the thesis of Gerald Leach et. al., who in 1979 had published ‘A low energy strategy for the UK’. That book, like the parallel but better known ‘Soft energy paths’ by Amory Lovins in the US, published in 1976, received much criticism and opprobrium from the energy establishment, which was of course heavily supply side dominated at the time. The government forecasts had UK energy demand growing dramatically, by 64% between 1976 and 2000. Looking back it turned out that reality turned out much closer to Leach’s scenarios than those of the energy establishment. (See ‘Surprise, you are living in a low energy future…(almost)’). Economic growth pretty much matched the forecasts but energy use hardly changed.

I was fortunate in many ways as a series of seemingly ‘random’ events took me to Stirling after a year of working doing energy audits. I moved to Stirling which has one of the most beautiful campuses in the world in late 1981. I didn’t think it was such a good idea when the first winter arrived with a shock, it was one of the coldest UK winters on records, with temperatures down to minus 15oC. The loch on campus froze over (see photo).

Having taken an unusual interdisciplinary degree about energy I continued my inter-disciplinary approach and my PhD was funded by a joint committee of the Science and Engineering Research Council and the Social Sciences Research Council. When doing a PhD the student-supervisor relationship is critical and my supervisor, Keith Jacques, was brilliant in many ways but eccentric. He had been an industrial chemist, developed some new materials and then somehow ended up as a school teacher and then University lecturer. He introduced me to soft systems thinking which was embedded into my research and I think has influenced nearly every project or job I have done ever since. For anyone not familiar with soft systems thinking check out ‘Systems Thinking, Systems Practice’ by Peter Checkland.

My work at Stirling was within the Technological Economics Research Unit (TERU), smaller but similar to Sussex’s SPRU, but with more emphasis on management of innovation and technology. A condition of doing my PhD was to take the taught part of the MSc Technological Economics so I spent my first 9 months in Stirling in a class of 12 students from 8 countries, (which was more unusual back then than it would be now), taking MSc courses similar to those on an MBA including Business Strategy, Operations Management, Statistics, Capital Budgeting, Accounting, Marketing etc and working on my PhD part time. Like most PhD students there were many, many times when I wondered what I was doing and considering going back to the world of work.

As my PhD evolved we settled on four industries to focus on – the ‘boozy’ ones of brewing, distilling, malting and dairies. The brewing industry had, and probably still has, the best industry wide records on energy performance and there is a close link between brewing and the study of energy. Joule’s discovery of the fundamental law that energy is always conserved was based on experiments undertaken in his father’s brewery. Sir Oliver Lyle’s classic work, ‘Efficient use of steam’, published in 1946, chose a brewery to demonstrate heat balances. Opening with the statement “The input of a brewery is cold water. The output is cold beer“, he then proceeded to examine why it is that a product which is as cold when it comes out of the brewery, as the water of which it is largely composed was when it went in, needs more energy than just the “necessary push to start things off”.

Much of my time was spent visiting many sites within those sectors with a strong emphasis on brewing – tough work but someone had to do it. You have to remember that in those days a) there were far more breweries than there are now, (excluding micro-breweries which hardly existed then) and b) it was not unusual to drink alcohol at lunch time even in production sites. I also spent an extended time working closely with the engineering team at Ind Coope Alloa which was a leader in energy management – led by the engineering manager Ray Banton. There I discovered that their innovative heat recovery system had been incorrectly installed and commissioned, and the team quickly put it right.

Much of my work focused on barriers to achieving the potential for energy efficiency, and how they could be overcome, something I still spend a lot of time thinking about and working on.

It also emphasized that many estimates of potential for energy efficiency under-estimated the specificity of each situation and the need to adapt a technology rather than just adopt it. Even off-the-shelf equipment has to be engineered to fit the specific application. For any particular technology, site specific technical, financial or management constraints will apply – even in something seemingly so simple as low energy lighting, which in those days did not of course include LEDs. This focus on the specificity and the importance of incremental technological change was recognised by the external examiner, the late Professor Chris Freemen of SPRU, as a major advance in innovation literature as well as energy efficiency literature. All too often talk of innovation focuses on the large, major changes as opposed to the less exciting, but often more impactful incremental changes and improvements.

Of course much has changed in four decades. First of all we have moved from talking about ‘energy conservation’ to ‘energy efficiency’. Secondly we have realized the threat of climate change and reduction of emissions has become a major motivator of investing in improving energy efficiency. There was no mention of carbon emissions reduction in the debate at all back then. We have had huge technological change, particularly around computing which was in its infancy in the 1980s, (I think my PhD was one of the last to be typed by a secretary as the University had only just adopted state of the art ‘word processors’). However, the fundamentals have not changed, the potential for cost-effectively improving energy efficiency remains similar in scale and energy efficiency is still insufficiently recognized in energy policy. Reducing energy costs remains important. Reducing reliance on imported energy is just as important. As I was reviewing some of the text for an update to my book ‘Energy Efficiency’ I thought I would explore some of the conclusions of my PhD and update them for today’s world in a mini-series of blogs to follow.

Monday 6 January 2025

Happy, healthy and successful New Year to all my readers. Given what is happening in Washington DC today I could not resist diving back into commenting on developments in the USA.

I was struck by several recent articles about the views of the nominee for US Energy Secretary Chris Wright. As has been widely reported he has said: “There is no climate crisis, and we’re not in the midst of an energy transition either”.

He has also claimed that any negative impacts of climate change are “clearly overwhelmed by the benefits of increasing energy consumption.” Given the importance of his future role, (subject to Senate confirmation), for the US, and global energy scene, I decided to do some more research for myself and went to the source. In 2024 Chris Wright’s oil services company, Liberty Energy, published a 177 page ‘Bettering Human Lives’ report1 which includes a lot of data and thought provoking analysis about the global energy picture.

Liberty Energy’s, and clearly Chris Wright’s, key takeaways are as follows:

- Energy is essential to life and the world needs more of it!

- The modern world today is powered by and made of hydrocarbons.

- Hydrocarbons are essential to improving the wealth, health, and life opportunities for the less energized seven billion people who aspire to be

- Hydrocarbons supply more than 80% of global energy and thousands of critical materials and products.

- The American Shale Revolution transformed energy markets, energy security, and geopolitics.

- Global demand for oil, natural gas, and coal are all at record levels and rising — no energy transition has begun.

- Modern alternatives, like solar and wind, provide only a part of electricity demand and do not replace the most critical uses of hydrocarbons. Energy dense, reliable nuclear could be more impactful.

- Making energy more expensive or unreliable compromises people, national security, and the environment.

- Climate change is a global challenge but is far from the world’s greatest threat to human life.

- Zero Energy Poverty by 2050 is a superior goal compared to Net Zero 2050.

Several of these points are indisputable. Throughout the report there is an emphasis on the link between energy use and economic development with all its massive benefits in health, education and welfare, and an admirable commitment, in words and actions through a Foundation, to reducing energy poverty and increase the use of clean cooking.

Overcoming energy poverty, and poverty in general, is without a doubt one of the major global challenges we face – we need to make everyone wealthier. But the argument that this can only be done by using more fossil fuels seems to be another example of the primary energy fallacy. It is not primary energy that drives development but rather the level of services being delivered, and those services need energy which can be delivered in different ways using different technologies. Take a remote village in a developing economy, it is clear that the people in the village want to have more lighting, which directly improves education and safety; more pumped water, which directly improves health, education and women’s safety; more cooling for AC and cold chains, which directly improves nutrition, health and incomes through reducing food loss; more computing and internet services which helps education, and farmers check prices, avoid middle-men and access markets; and more mobility for commerce and leisure. These are all services that require energy input. The point is that we do have a choice over the technologies we use to provide them.

We can either hook them up to a conventional grid or provide a local fossil fuel generator, or we can install solar, batteries, LED lighting, micro-grids, induction cooking and efficient cooling systems. The first has a capex, takes money out of the local economy, exposes people to volatile fuel prices, and produces carbon emissions, and air pollution. The second version still requires capex of course, but has no fuel costs, no exposure to volatile energy prices, and produces no carbon emissions or air pollution. Are the people of the village better or worse off? At a very real level they don’t care where their energy come from, they just want more services at the lowest cost. Chris Wright’s view is that the lowest cost always comes from fossil fuels but, even ignoring externalities, the rapidly falling cost of solar, batteries and related technologies make this at least questionable – and something that should be questioned in every situation.

Of course we may not be able to provide 100% of those energy services in the renewable scenario in all cases quite yet, but there is more evidence that we can and are increasingly likely to be able to do it routinely at less cost than the fossil fuel/grid approach. Work in India and elsewhere demonstrate that the rapid declines in the cost of solar and batteries can mean that the total delivered energy cost can be less than that of connecting to the grid.

The Bettering Human Lives report goes on to say:

‘The reality is that these politically favored technologies’ [referring to renewables and batteries] ‘have not, will not, and cannot replace most of the energy services and raw materials provided by hydrocarbons. Today they are deployed almost exclusively in the electricity sector, which delivers only 20% of total primary energy consumption. Manufacturing is the largest user of energy globally, mostly in the form of process heat that cannot effectively be supplied via electricity’.

Well of course it is true that renewables and batteries are mainly in the electricity sector. But here again we see the primary energy fallacy, we should be focused on end-use energy not primary energy. Also the statement about manufacturing process heat is rapidly being overtaken by events, at least for low and medium-temperature process heat, with electrification and heat pumps increasingly being deployed into these applications. Industrial heat pumps are well suited to many applications in the food and beverage, pulp and paper, and chemicals sectors, which collectively account for c.15% of global industrial emissions. McKinsey expect the market for industrial heat pumps to grow at more than 15% per annum up until 20302. At the moment most of the installations are up to 5 MWt but the trend is towards larger machines and higher temperatures. A 2024 study by Fraunhofer ISI showed that more than 60% of EU industrial heat demand could, in theory, be met by electrification and that with technologies that will be available by 2035 this could rise to more than 90%3. Now, having written my PhD on the potential for energy efficiency in industry I am the first one to challenge the definition of potentials, technical potentials are definitely not the same as economic potentials, which are not the same as achievable potentials, but the opportunity is clear. When we look at investment decisions being made we see signs of real investment in these technologies happening, examples include:

UPM announced it will install eight 50-60 MW electrode high pressure steam boilers across paper mills in Germany and France4 .

A pilot electric steam cracker in a BASF refinery that produces the 850oC temperature to produce ethylene has gone into operation, the technology has been developed in a collaboration between BASF, Linde and Sabic5.

According to data from Global Energy Monitor’s (GEM) Global Steel Plant Tracker, 93% of the new steel plant capacity announced in 2023 was for electric arc furnace (EAF). According to GEM this is part of ‘a transition away from coal based steel making’ and that if these developments and planned retirements take effect ‘global operating steel capacity should sit just under the IEA’s net zero-aligned target of 37% EAF steelmaking by 2030, and with heightened momentum the goal is increasingly attainable’6 .

A 2 MWh heat energy battery is supplying 1,000oC heat to an ethanol plant in California on a commercial Heat-as-a-Service (HaaS) basis, supplying energy at a cost per MMBtu lower than gas-fired heat7 .

It is true that some of these developments, like the electric steam cracker, are being supported by governments or concessionary finance and that the viability of electrification depends on the relative price of power to fuels but the trends are clear.

The Liberty Energy report also says:

aviation, global shipping, long-haul trucking, and mobile mining equipment have no viable replacements in sight.

With the rapid developments in electric heavy goods vehicles8, and a good economic case, it is clear that EHGVs are the future9, we will of course need more investment in the rapid charging network but that is starting to happen10. As for mining equipment, in December 2024 Australian mining company Fortescue placed a $400m order for more than 100 electric mining vehicles with Chinese manufacturer XCMG11. This order follows a $2.8 billion deal with Liebherr for 360 autonomous electric trucks, 55 electric excavators and 60 electric dozers in September 2024 and a deal to buy 30 electric graders in October 2024 from Canadian manufacturer Maclean. Fortescue has invested heavily in developing its own electric vehicle technology which will be incorporated into these machines12. Aviation and shipping are more difficult of course but again progress is being made in electrification and alternative fuels.

The Bettering Human Lives report goes on to say:

Some retort that we don’t need more energy, we just need to use energy more efficiently. The pioneering 19th century English Economist, William Stanley Jevons, addressed this conjecture in his 1865 book The Coal Question. He concluded that increases in energy efficiency led to more, not less, coal consumption.

[referring to a graph] we can see two centuries of increasing efficiency in energy usage to generate economic value (GDP) combined with two centuries of growing demand for energy. Since 1990, energy efficiency has increased 36% and total energy consumption has increased 63%.

There is no highly energized poor country, and no low-energized rich country. Health, prosperity, and opportunity require energy.

Just how bad these energy and climate policy decisions are can be gauged by falling energy consumption in many Western countries. In the United Kingdom, energy use has fallen by 30% to levels not seen since the 1950s, while the rest of Europe has declined to 1990s levels. British electricity consumption, amazingly, has fallen by about a quarter since 2003 and is now back at levels last seen in the late 1980s.

I have addressed the Jevons paradox too many times to do it again here, it resurfaces about every decade and is often mis-used. The literature is extensive. Yes of course there is a rebound effect but it is less than one. The really interesting graph is what our energy use would have been if we had maintained the same energy intensity as in the 1970s. See page 5 of the 2012 ACEE report by Skip Laitner et.al13.

As for the statement about there being no highly energized poor country and no low-energized rich country this again makes the primary energy fallacy. Energy intensity is a matter of technology choice. Denmark for instance aggressively introduced energy efficiency and wind power after the oil crises14 and in 2023 wind made up 58% of total generation15. You cannot say that Denmark is a poor country.

It is true of course that UK energy use has fallen by 30% to levels not seen since the 1950s and that electricity consumption is now at levels last seen in the late 1980s. But in those time periods the adoption of energy using appliances, central heating, cars, foreign holidays etc. has grown enormously – as has GDP. We are not less well off because energy use has fallen. We may be less well off than we could have been because of many factors, including the price of energy, but much of the change has happened through improved efficiency and changes in underlying technologies.

The nominee Secretary of Energy’s thinking seems to mirror the prevailing views of the late 1970s and early 1980s when I first studied the energy system. Then forecasts, global and national, all showed ever increasing energy use as GDP increased – the underlying assumption was that the relationship between energy use and GDP was fixed. Forty years on we have seen economic growth but energy use has not risen in step. In fact in the US and the UK energy use has remained nearly constant despite forty years of economic growth – as I wrote in 2013, we are living in what in the early 1980s was considered by nearly all experts and energy industry gurus as a totally impossible ‘low energy future’ – and we did it almost without trying16. The relationship between energy use and GDP has changed because of the effect of energy efficiency and changes in industrial structure. What’s more the relationship between GDP and fossil fuel use is changing because of the rise of renewables. We can decouple fossil fuel energy use and GDP. Our energy statistics system, established as it was in the fossil fuel age, with its focus on primary energy and millions of tonnes of oil equivalent does not help our understanding.

These energy supply dominated views still all too often dominate the energy debate and energy policy. Whether they are simply because people have not changed their views, or are examples of people ‘talking their own book’, who knows. The nominee does at least have a technical energy background and experience investing in alternatives such as geothermal and fusion power, which is a positive.

We do need to acknowledge the reality of our dependence on petrochemical derived materials and fertilisers, and ask ourselves the tough question whether alternatives are realistic. We cannot argue with the fact that hydrocarbons have delivered most of the improvement in economic well being, health etc. to date – but that was the past, it does not mean the future will be the same. There are two clearly competing world views here – one being the ‘you can only drive economic development with more fossil fuels’, the other being ‘you can drive economic development with energy efficiency and renewables’. Time will tell which of the competing world views is correct.

References

- http://libertyenergy.com/wp-content/uploads/2024/02/Bettering-Human-Lives-2024-Web-Liberty-Energy.pdf

- https://www.mckinsey.com/industries/industrials-and-electronics/our-insights/industrial-heat-pumps-five-considerations-for-future-growth

- https://www.agora-industry.org/fileadmin/Projects/2023/2023-20_IND_Electrification_Industrial_Heat/A-IND_329_04_Electrification_Industrial_Heat_WEB.pdf

- https://www.upm.com/about-us/for-media/releases/2023/04/upm-electrifies-heat-and-steam-production-at-its-mills-in-finland-and-germany/

- https://www.chemistryworld.com/news/basfs-electric-cracker-demonstrator-goes-online/4019439.article

- https://globalenergymonitor.org/report/pedal-to-the-metal-2024/

- https://rondo.com/calgren-case-study

- For example: https://www.scania.com/group/en/home/products-and-services/trucks/battery-electric-truck.html

- https://electriccarguide.co.uk/the-electric-hgv-guide/

- For example: https://www.pragmacharge.com

- https://www.electrive.com/2024/11/28/fortescue-orders-xcmg-electric-mining-equipment-worth-400-million/

- https://zero.fortescue.com/en

- http://www.garrisoninstitute.org/downloads/ecology/cmb/Laitner_Long-Term_E_E_Potential.pdf

- https://www.whatthedenmark.com/blog-post/green-transition

- https://www.iea.org/countries/denmark/energy-mix

- https://www.onlyelevenpercent.com/surprise-you-are-living-in-a-low-energy-future-almost/

Wednesday 27 November 2024

Well clearly the US election did not go the way I thought or hoped it would. The result will affect us all for many years in many ways, but none of them are likely to be good. I wrote about how I felt about the 2016 election here and right now I can’t add to that right now. I have made a decision to move on and spend less time reading and thinking about US politics, even though it is a life-long interest. I will just take action where I can. I started by acting on my belief in the power of impact investing, impact managing and impact consuming by coming off of X and moving my social media activity to Blue Sky. It is impossible for me to support any of Elon Musk’s businesses as he is clearly anti-democracy and many other things I don’t agree with.

Anyway as part of moving on I am now re-focused on working, writing and speaking to help accelerate the very necessary transition to a net zero and regenerative world. To that end ep is working on a number of projects including: our Net Zero Delivery Vehicle, an innovative public-private partnership to bridge the development gap between good ideas and bankable, large-scale, systematic net zero projects; a project working on distributed energy solutions in Ukraine; and ep Assets move into delivering distributed energy projects in the UK in response to client demand. We announced a partnership with Pixii, the fastest growing technology company in Norway in 2023, to introduce their Pixii box technology and energy storage solutions to the UK. ZPN Energy, where I am non-exec Chair, is rolling out its battery backed rapid EV chargers and mobile charging solutions. At CBHH we continue to raise capital for impactful energy transition and natural capital companies.

It is clear that electrification, and particularly distributed energy systems using solar PV, batteries, EV charging and flexibility is the next phase of the energy transition – driven by the drive to decarbonisation, economics, power supply constraints, and a desire for higher levels of resilience. The impact of this change will be massive and produce much higher levels of overall energy efficiency as fossil fuel use is displaced. It will also require us to move on in our thinking in several ways. Firstly all building and facility owners need to think of themselves as energy producers as well as consumers – the now over-used word prosumer applies. We are no longer just consumers and we need to take responsibility for our own energy generation and use as far as possible. At ep we believe all buildings should be power stations, producing power as well as providing ancillary services in the various grid support markets.

Secondly we need to re-think ‘energy’. Since the 1970s energy has been used in a way that confuses fuel and electricity. We need to make the distinction clear again, electricity is very different to fuel. Try putting fuel into an electrical device, or try putting electricity into your internal combustion engine car. Electrification, switching from fuel driven heating or mobility, to a low or zero carbon electricity grid, or a local micro-grid, results in so many benefits at all levels including big reductions in emissions.

Thirdly we need to think in new ways about energy statistics. We need to think about the quantity of energy services being delivered, it is that quantity that will be linked to wealth and GDP, not the level of primary energy being used. Memes on the internet saying something like there are no rich low energy countries, primarily being used to push a fossil fuel or nuclear agenda, are meaningless. Energy intensity, as measured by primary energy, will fall rapidly as more and more energy i.e. electricity, is generated close to where it is used, and metered energy taken from the grid falls; it will also fall as high efficiency electrical heating and mobility displaces low efficiency fossil fuelled systems in heating and transport. As I have said before, the level of energy efficiency in the economy is a choice, it is just a choice that we have generally made without thinking about it.

Despite the undoubtedly chaotic efforts of the incoming US Administration, and other wannabe dictators around the world, I believe the energy transition and particularly the move towards distributed solar and batteries will prove to be unstoppable. Their efforts to protect incumbent fossil fuel interests may delay things but at the end of the day they are dinosaurs looking up as the giant asteroid approaches.

In other news my 2013 book ‘Energy Efficiency. The Definitive Guide to the Cheapest, Cleanest, Fastest Source of Energy’ is now out in paperback at a reasonable price, available from the publisher, all good book sellers and Amazon. It has stood the test of time well as a broad introduction to the subject but I am working on what will be a companion book, revisiting the subject and looking at some of the major changes that have happened in the last decade, notably the advent of cheap solar and batteries, and the growth of interest and activity in financing energy efficiency. I also published a collection of blogs from the first ten years of onlyelevenpercent.com – available on Amazon.

The title of this blog comes from the lyrics of ‘Move On’ by David Bowie

Saturday 26 October 2024

The news that Jeff Bezos has stopped the editorial board of the Washington Post from publishing an endorsement of Kamala Harris reminded me of a piece I wrote back in 2021 entitled ‘Upstanding and Bystanding – Time for some Personal Corporate Social Responsibility’, which seems even more relevant now. This was inspired by a visit to the Dallas Holocaust Museum which categorised people during the holocaust as; perpetrators; bystanders; upstanders and of course victims.

It is clear, as it has been for a long time, that Donald Trump is a narcissistic psychopath who is threat to democracy, the rule of law, the global economy and global security, as well as many other bad things. He has created a cult that supports him, aided and abetted by Republican politicians like Mitch McConnell and many others who made the decision that supporting Trump was in their best interest, even though they knew full well what he was like and what he stood for. Even if they are not direct perpetrators they are collaborators.

The events in the USA since 2016 demonstrate clearly how any country can slowly slide towards authoritarianism, and answers once and for all the old question: how did Hitler and the Nazis came to power in pre-WW2 Germany? The process must have been very similar. Now we have leading newspapers, the Washington Post and the LA Times, spiking endorsements because their owners don’t want to upset Trump. If Trump is elected, next they will be publishing positive pieces about him and spinning news stories to make him look good. What comes after that? Amazon sourcing and delivering the modern equivalent of SS uniforms or AWS providing data services for the equivalent of the Stasi Records Agency?

The real irony of course is that The Washington Post is the newspaper that broke the Watergate story, and that four years after the takeover by Jeff Bezos the paper adopted the masthead ‘Democracy dies in darkness’. Bezos has at the very least dimmed the lights on democracy.

The original piece is here.

https://www.onlyelevenpercent.com/upstanding-and-bystanding-time-for-some-personal-corporate-social-responsibility/

Dr Steven Fawkes

Welcome to my blog on energy efficiency and energy efficiency financing. The first question people ask is why my blog is called 'only eleven percent' - the answer is here. I look forward to engaging with you!

Get in touch

Email notifications

Receive an email every time something new is posted on the blog

Tag cloud

Black & Veatch Building technologies Caludie Haignere China Climate co-benefits David Cameron E.On EDF EDF Pulse awards Emissions Energy Energy Bill Energy Efficiency Energy Efficiency Mission energy security Environment Europe FERC Finance Fusion Government Henri Proglio innovation Innovation Gateway investment in energy Investor Confidence Project Investors Jevons paradox M&V Management net zero new technology NorthWestern Energy Stakeholders Nuclear Prime Minister RBS renewables Research survey Technology uk energy policy US USA Wind farmsMy latest entries