Tuesday 2 February 2016

Like many others I have long been troubled by the UK government’s decision to support new nuclear and particularly by the bizarre decision to guarantee the Hinkley C project by agreeing a strike price of £92.50/MWh and up to £17 billion in Treasury loan guarantees. I have never been against nuclear power per se although I have serious questions about the choice of basic technology, (uranium cycle pressurized water reactors), and the risks of failure in very complex systems where the consequences of failure can be huge. I do worry about the wisdom of choosing a reactor design where the two other examples are hugely over-budget and behind schedule. I seriously worry about relying on Chinese funding and Chinese technology to build future reactors.

Having read a piece in the Sunday Times (“New threat to Hinkley nuclear plant cash”), I am now less worried because it looks less likely that the project will ever go ahead. The “new” (not actually that new) information is that the EU’s approval of the Treasury’s guarantee is dependent on the French reactor at Flamanville having “completed the trial operation period” and other operational milestones by December 2020. In September 2015 EDF announced that the Flamanville start-up was now scheduled for Q4 2018 – the latest in a long-line of delays (as well as budget increases). Even if the French regulator does not force EDF to remove the steel containment vessel, which has been found to have “anomalies” and “lower than expected mechanical toughness values”, I have no confidence in their ability to meet this target given their inability to meet any of the previous ones.

The decision from the regulator on the pressure vessel may not even come until the end of 2016. Even if EDF hit the Q4 2018 target (a big if) that only leaves 24 months to satisfy the EU’s conditions. So, in my opinion, Hinkley will never get built and prove to be the biggest in a long line of UK energy policy mistakes (and no doubt the tax payer will end up picking up the bill in some way). So, time to stop worrying about Hinkley and worry about how to really solve the problem of the short and medium-term electricity capacity shortage caused by years of inaction by successive governments. The answer is not new nuclear and it is not subsidizing fleets of polluting diesel generators (which we are doing) – the demand side of the answer lies in properly valuing all the multiple benefits of efficiency and making it measurable and an investable asset class, as well as reforming the energy market to allow efficiency to properly compete with supply.

Tuesday 12 January 2016

It would be impossible for me not to comment on the terribly sad death of David Bowie. As for many of my generation he was, and remains, a big part of my life and is by a very long way my favourite musician of all time. His influence on music, art and culture cannot be under-estimated. Perhaps it can only really be appreciated by those of us who were there and watched the 1972 performance of “Starman” on Top of the Pops on black and white TV, under the dis-approving parental gaze. The world changed at that moment.

In 1976 I was lucky enough to win tickets to see the world premier of his first film, “The Man Who Fell to Earth”. Apart from the excitement of attending a star studded (minus Bowie) world premier I will never forget the first shot of him on the big screen in Leicester Square or the impact of the movie. I still have the ticket and the movie poster, bought for the then not inconsiderable sum of 50p.

I first saw him live on the “white light” Isolar II tour in June 1978. A friend and I managed to get to the front row centre stage, no more than a couple of metres away from Bowie. Subsequent concerts in stadia, The Glass Spiders tour in June 1987 at Wembley, and the Sound+Vision tour in August 1990, were great but could never beat being in the front row of the New Bingley Hall County Showground in Stafford.

So what was/is the appeal of Bowie? For those who know of my interest in space it will not be a surprise that the space and science-fiction nature of “Ziggy Stardust & the Spiders from Mars” was the original draw for me. It soon went far beyond that as his lyrics always seemed to have great meaning about life, love and the universe. As the cliché goes he always innovated and it seems hard to believe that fans, me included, who loved the sci-fi rock of “Ziggy Stardust” could also like what Bowie called the plastic soul of “Young Americans”, the indefinable “Station to Station”, the techno “Low”, and the dance music of “Let’s Dance”. There was always that period of adjustment to the new style when a new album came out but with the exception of a few albums they all came good in the end. Even the low points had their moments of brilliance.

As well as the changes in style he was always at the cutting edge of musical experimentation and technology, and then later video and the internet. In a 2000 interview with Jeremy Paxman he talked about the power of the internet to disintermediate and break down the barrier between the artist and the consumer. It is hard to remember the primitive nature of the internet in 2000 but Paxman’s reaction and look of skepticism expresses it well. Now of course, 16 years later, we take disintermediation and “prosuming” as the norm, and the kind of music and video technology that used to cost a fortune is now available in apps that cost pennies or are even free – meaning anyone can create professional quality music, video and art.

Without a doubt David Bowie was a creative genius, but perhaps more importantly one who was able to channel that creativity into action without worrying about the barriers or what people will think. We are not all musical, (I know I am not) but we are all more creative than we think, but we allow lots of barriers to get in the way of creating so Bowie’s life should inspire us to always act on the creative drive. His music, film, art and effect on culture will live on forever. As he said in “Quicksand”:

“I’m not a prophet or a stone age man

Just a mortal with the potential of a superman.”

Monday 21 December 2015

The end of the year always brings the pressure of whether or not to write something seasonal. This year I thought I would do something different by formulating my Laws of Energy Efficiency. Sir Isaac Newton and the Arthur C. Clarke stopped at three Laws so I apologize for coming up with 12. They echo some of the themes I have covered in the blog over the last three years.

- Energy efficiency is boring and seriously uncool to most people most of the time.

- Never talk about energy efficiency without mentioning the non-energy benefits which can be seriously cool.

- Talk about energy productivity and not energy efficiency.

- If you are supposed to be an energy journalist never headline a story about renewables with something about “energy efficiency”.

- If you put ten people from ten ESCOs in a room there will be 15 different definitions of what an ESCO is.

- If you have five energy auditors survey any building you will end up with reports in five different formats with savings calculated five different ways, even if they are all recommending the same measures.

- Energy Performance Contracts and ESCOs are not the magic bullet some enthusiasts and failed investment bankers looking for the next big thing think they are.

- Never call energy efficiency a “no brainer” or “low hanging fruit”.

- An exciting energy or energy efficiency discovery in a lab somewhere is not the same as a viable technology, which is not the same as a commercial product, which is not the same as a successful product that has meaningful impact in the world.

- Any politician who finishes an energy speech by saying “and don’t forget energy efficiency” will promptly forget it the next time he or she meets an energy supply lobbyist.

- Energy forecasting is easy, getting it right is difficult. The corollary to this law is that prices can go down as well as up – never forget that in 1986 oil went below $10/barrel oil only months after oil industry bosses said “oil will never sell for less than $20/barrel again” and “our doomsday forecast is $20-25 a barrel”.

- When a distinguished but elderly economist says “what about the Jevons Paradox”, ask him or her if they think improving productivity is a bad idea.

Thanks for reading onlyelevenpercent.com.

Have a Happy Christmas and a healthy, prosperous and energy productive 2016.

Monday 14 December 2015

For those of us who have worked in energy efficiency a long time it sometimes seems as if the moment has come, the moment when the world has finally recognized the value of improving efficiency, the fact that there is huge potential which is economic today using today’s technologies with no subsidies, and that improving energy efficiency brings with it massive non-energy benefits such as job creation, productivity and improved health and well being. All, and I say all lightly as it is no small task, we need to do now is work out how take advantage of that huge economic potential that we know is out there. We are advancing quickly on that journey with projects like the Investor Confidence Project, the continuation of the work of the Energy Efficiency Financial Institutions Group (EEFIG) on establishing a common under-writing framework for energy efficiency (supported by the EU), and new business models. An increasing amount of capital is committed to finding ways of investing into efficiency – now we just need to make it possible for that investment to flow by breaking down the institutional and cultural barriers.

In the UK the energy policy reset has dealt with supply options (mainly promoting new nuclear and shale gas) but remains silent on efficiency. For the record I am against new nuclear (especially with unproven French or Chinese technology) because of cost and security concerns. I am in favour of shale gas on energy security grounds assuming we can exploit it cheaply. In any event, these supply options will take at least a decade (almost certainly more in the case of new nuclear) to take effect. Meanwhile we are sitting on a huge reserve of very cost-effective energy efficiency potential that is not being exploited and which could be unlocked very quickly. Almost every day we see cases of buildings, in some cases very new buildings, making savings of 10 to 30%, often with little or no investment. Everyone talks about the declining cost of solar but we also need to recognize the declining cost of delivering efficiency. We need to build on that base of activity and accelerate demand, supply and financing of efficiency and hence rebalance the emphasis on supply options.

One way of doing that may be to stop using the term energy efficiency all together. Having worked in the field for so long, and finally having the subject get more recognition, this may seem like a strange proposal but energy efficiency has all kinds of problems as a label. It is a confusing technical term, it is boring to most people, it still has negative connotations of saving and getting by on less, it threatens energy suppliers, it is invisible, it does not lend itself to photo opportunities and big political announcements, and it leads to all kinds of pointless, endlessly resurfacing, debates based on the Jevons paradox.

We need to truly reset energy policy and focus on energy productivity –the amount of value we create out of a given amount of energy (GDP/energy input). Productivity is positive. Improving productivity generates wealth. No-one can be against improving productivity. Of course for any particular country energy productivity is made up of two elements, the overall structure of industry and the economy, and the level of actual energy efficiency.

In the UK tackling the country’s poor productivity record is core to the Chancellor’s economic strategy – we need to make sure energy productivity is part of that discussion and so far it clearly isn’t.

In July the Treasury published a document, “Fixing the Foundations: Creating a More Prosperous Nation”. Chapter 6 is called “Reliable and low-carbon energy at a price we can afford”. This does start by talking about “improving productivity in energy generation, production, supply and usage” (a good start). It then goes on to talk about more competitive markets and introducing the ability to switch suppliers within 24 hours. Competitive markets are generally good but the problem we have is that energy efficiency cannot compete with energy supply – there is no market for efficiency, only markets for stuff that results in efficiency. We now have the technology to meter efficiency and California is moving towards a market where efficiency can be measured, metered and truly compete in the energy market. We are developing new business models based on this idea. Personally I fail to see how 24 hour switching contributes to productivity. The rest of the points in this chapter mention supply, oil and gas, shale, new nuclear, and the EU’s Energy Union. In a strange final bullet point printed in red the now on-going review of business energy tax was flagged. It is almost as if they ran out of ideas and this chapter wasn’t quite finished.

So, apart from the statement “improving productivity in energy generation, production, supply and usage” there is no mention of productivity and no linkage to overall energy productivity – and no mention of energy efficiency. Efficiency is mentioned in the chapter on Planning and housing – flagging the decision not to proceed with zero carbon homes and saying they will keep energy efficiency standards under review. The energy chapter is the old 1970s style supply side dominated model in new clothes – “the economy will grow and we will provide whatever energy we need” – rather than focusing on improving energy productivity.

We need to start talking about energy productivity at the macro and the micro level, recognize the economic benefits that come from improved energy productivity (arising from energy cost savings, improved energy security, improved health, reduced need to invest in new supply options etc etc), and set national targets for energy productivity. To support that we need to aggressively promote energy efficiency (that is to say energy productivity at plant and building level) and really start to exploit the massive cost-effective energy reserve the efficiency potential represents, a reserve which is cheaper than any supply-side option, faster to bring on-stream, and by far cleaner than any other option.

So maybe we shouldn’t forget about energy efficiency all together, just rename it energy productivity.

Fixing the Foundations can be found at:

Information on the Investor Confidence Project:

The EEFIG report can be found at:

http://www.unepfi.org/fileadmin/documents/EnergyEfficiency-Buildings_Industry_SMEs.pdf

Thursday 26 November 2015

An edited version of my panel presentation at the Building Energy Symposium, Lisbon, Portugal, 24-25 November 2015.

I have always been a student of the future. I grew up in the 1960s in the midst of the space race and started a life long passion for space and science fiction. When you read science fiction long enough you realize that it has a habit of coming true – just think about the mobile phone or video calls, not so long ago they were the realm of science fiction and now they are part of everyday life.

My favorite science fiction writer Arthur C. Clarke once said that we tend to over-estimate what we can achieve in the short-term and under-estimate what we can achieve in the long-term. Nowadays it seems as if the long-term has been dramatically shortened – it is only eight years since the launch of the iPhone and in that time smart phones have become the norm. Arthur C. Clarke also said “the future isn’t what it used to be” – which I now take to mean that we have become pessimistic about the future with dystopian scenarios of over-population, resource depletion and environmental degradation becoming prominent. Personally I am an optimist and think we can and will solve those problems – and energy efficient building renovation is the one of the best ways of addressing the energy related problems we face.

The focus of this panel is the future and that always starts people thinking about new technologies. It is important to be crystal clear that we can make significant (20 to 40% or more) energy savings in our buildings cost-effectively without any new technology. Today we have seen several case studies that demonstrate this, including the impressive results achieved by Sonae Sierra in shopping malls. And there are many more out there. Accelerating the rate of energy efficient renovation, something we must do to resolve our energy problems of costs, security and environmental impact, is not a technology problem it is a management and institutional problem. Don’t mis-understand me, we will always have new technologies emerging and they will help to make energy efficiency easier and cheaper, expanding the massive cost-effective resource that energy efficiency represents. Innovations like factory made retrofit kits will have a massive impact. But where we really need innovation is in processes, management, institutions and finance.

A lot of investors and lenders want to deploy money into energy efficiency as they have realized it is profitable, a big potential market and not dependent on subsidies. At the moment many of them are working out how to deploy capital and several existing funds have had problems getting money out of the door.

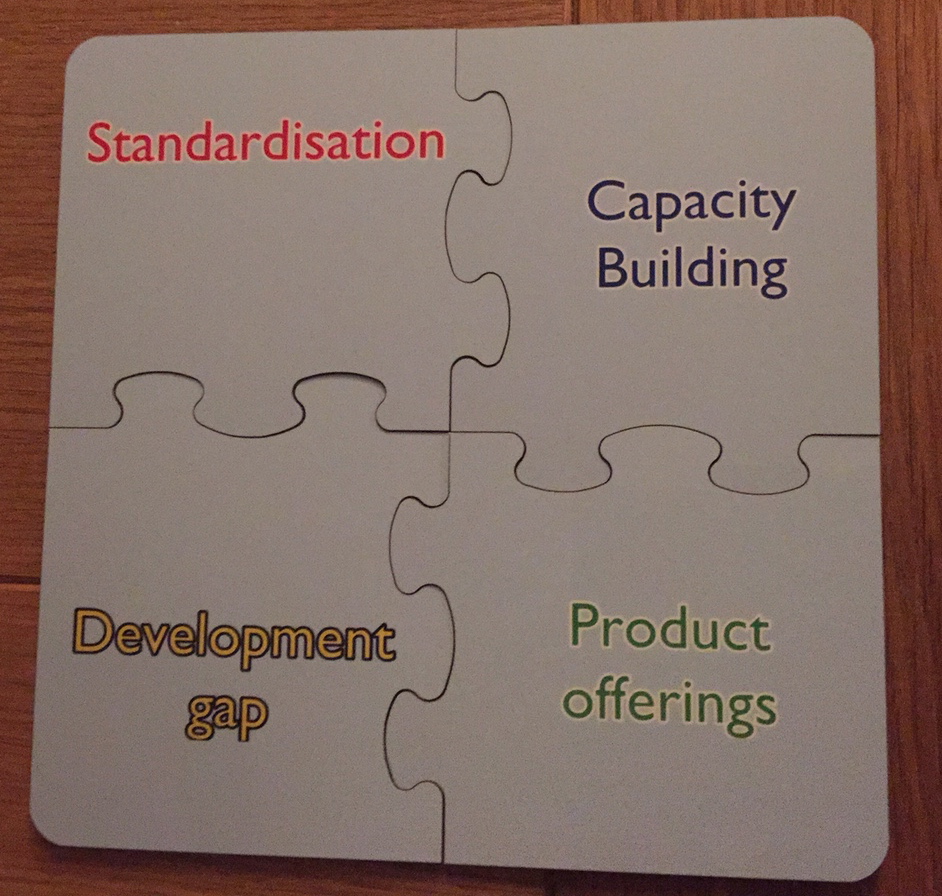

In order to scale up investment into energy efficiency we need to think about the problem like a jigsaw, to complete a jigsaw you need all the pieces not just one or two. The key piece in this jigsaw is standardization of the development and documentation of energy efficiency projects – and this is where the Investor Confidence Project comes in. If you develop a wind farm project you have to follow standard processes and produce standardized documents whereas in energy efficiency everyone does it differently. This causes a number of problems for banks and investors, namely: increased risks due to uncertain project performance, higher due diligence costs, inability to aggregate projects, and inability to build teams around standard processes. The lack of standardization has been identified as a major barrier by the Energy Efficiency Financial Institutions Group (EEFIG) and others including the IEA and Citibank.

The Investor Confidence Project (ICP) is a way of addressing this problem. It started in the US and we brought it to Europe with the help of Horizon 2020. Working with investors and lenders and the energy efficiency industry, the ICP has developed a set of Protocols that set out how to develop and document EE projects in buildings. The Protocols cover apartment buildings & tertiary buildings. It is important to understand that the Protocols are not about inventing new standards, we have lots of technical standards, but rather about standardizing the process and the document set. The Protocols are now available on the website – europe.eeperformance.org – and we are now working with pilot projects across Europe including Porto Viva (the city wide renovation programme in Porto), to embed the Protocols into project development .

If you have projects that would benefit from ICP and becoming more attractive to private capital we would happily discuss how we can help you. Please join as an Ally or join the Technical Forum that is overseeing the development of the Protocols – it is free.

Another important part of the jigsaw is capacity building and this has to be in three areas.

– in financial institutions. The EIB has an on-going project to train banks in energy efficiency projects and the EU has a new project to help develop standardized under-writing procedures using the ICP as a foundation.

– on the supply side i.e. the energy efficiency industry. We need to develop better skills in integrated design and build supply chains that can deliver whole building retrofits.

– on the demand side i.e. the building owners. We need to make owners more aware of the benefits of energy efficiency and particularly non-energy benefits (NEBs). NEBs are growing in importance and are much more exciting that energy saving. Energy efficiency is boring, they include things like health, welfare, additional revenue and economic development. Much work is now going on to value these non-energy benefits. They are much more strategic and exciting to decision makers than energy efficiency and cost savings. We need to talk about the NEBs every time energy efficiency is mentioned.

Another important part of the jigsaw is product offerings – the propositions offered by the energy efficiency industry. For many years people have talked about Energy Performance Contracts (EPCs) but they have never really taken off except perhaps in the public sector. We need to accept the limitations of the EPC product and start to innovate new models. In general, at corporate and policy levels, we need to switch to a “pay for performance” model where contractors get rewarded for actual delivered energy savings relative to the baseline consumption. At the moment we have business models and policies that reward buying stuff with no regard to the actual savings achieved by the investment. We now have the technology to measure these savings or negawatt hours. Switching from a “pay for stuff” to a “pay for performance” model allows all kinds of interesting new business models where producing energy efficiency suddenly becomes a revenue stream, and revenues are always more interesting than cost savings. California has embarked on this switch, if we in Europe can do the same my prediction for the future is that we will be amazed at the results. We can cut building energy consumption, cut costs for owners, reduce local and global environmental impacts, and reduce Europe’s massive energy import bill which is over €1 billion a day.

Thank you.

Thanks to VIDA IMOBILIÁRIA for the invitation to speak and revisit a great city.

Dr Steven Fawkes

Welcome to my blog on energy efficiency and energy efficiency financing. The first question people ask is why my blog is called 'only eleven percent' - the answer is here. I look forward to engaging with you!

Get in touch

Tag cloud

Black & Veatch Building technologies Caludie Haignere China Climate co-benefits David Cameron E.On EDF EDF Pulse awards Emissions Energy Energy Bill Energy Efficiency Energy Efficiency Mission energy security Environment Europe FERC Finance Fusion Government Henri Proglio innovation Innovation Gateway investment in energy Investor Confidence Project Investors Jevons paradox M&V Management net zero new technology NorthWestern Energy Stakeholders Nuclear Prime Minister RBS renewables Research survey Technology uk energy policy US USA Wind farmsMy latest entries

- A look back at the last forty years of the energy transition and a look forward to the next forty years

- Domains of Power

- Ethical AI: or ‘Open the Pod Bay Doors HAL’

- ‘This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning’

- You ain’t seen nothing yet

- Are energy engineers fighting the last war?

- Book review: ‘Stellar’ by James Arbib and Tony Seba